About Konsento

Konsento is an independent Swiss LegalTech platform that digitizes and simplifies legal processes relating to share capital. Since 2021, we have been supporting Swiss SMEs — from startups to established companies — in the efficient, legally compliant processing of share registers, general meetings, board meetings and capital increases.

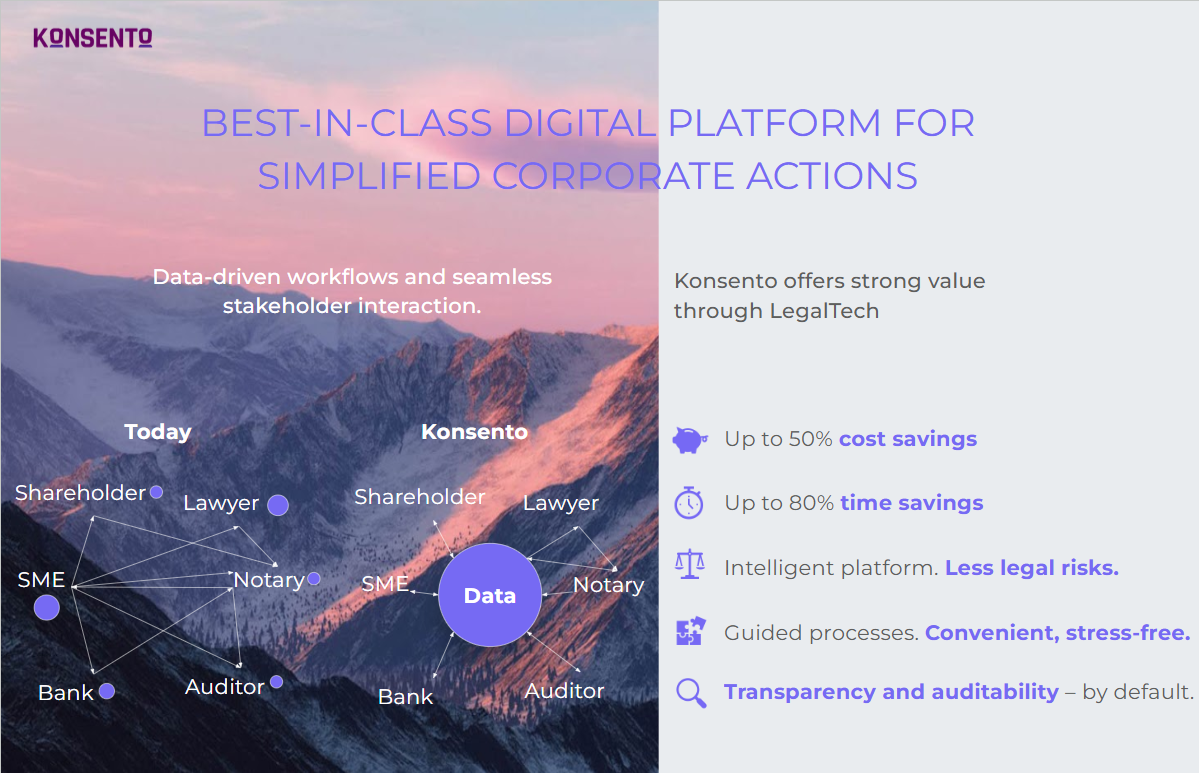

Our intelligent platform connects founders, boards of directors, shareholders and external service providers such as notaries or auditors in a secure, structured workflow. Developed by an interdisciplinary team of lawyers, IT and finance specialists, continuously optimized for seamless corporate actions.

Already implemented:

350+ general meetings

100+ Corporate Actions

21,000+ users — especially shareholders and participants

More than 450 Swiss stock companies rely on Konsento — for greater clarity, security and efficiency in equity management.

Simplify legal workflows and focus on what matters.

Konsento is the intuitive governance platform that helps you stay compliant, in control, and one step ahead. With powerful tools tailored to Swiss stock corporations, you can simplify complex legal tasks and act with confidence.

Our customers report massive time savings in all relevant corporate actions.

Fewer legal risks thanks to clearly managed processes and integrated legal logic.

Get to know the experts behind Konsento

550+ Aktiengesellschaften vertrauen uns

Gain peace of mind by simplifying complex governance tasks.

Trusted by 450+ Swiss stock corporations and 21'000+ users

From early-stage startups to established listed companies.

Dietmar Hold

Dietmar Hold

CCO, co-founder

Thomas Steinmüller

Thomas Steinmüller

CEO, co-founder

Alan Frei

Alan Frei

Founder & CEO

Thierry Kneissler

Thierry Kneissler

Chairman of the Board

Michael Borter

Michael Borter

Founder & CEO

Frequently asked questions

Which documents should a bank additionally request for domiciliary companies?

In addition to Form A, it is advisable to obtain the documentation of the enquiries into beneficial ownership and a depiction of the control chain, so that the bank can classify discrepancies between Form A and the Transparency Register beyond doubt and either substantiate any discrepancy notification or demonstrate that the exception applies.

Must a difference arising from anti-money laundering law be reported?

No. Discrepancies arising from diverging provisions of anti-money laundering legislation, in particular from the definition of the beneficial owner of a domiciliary company, are exempted from the obligation to report discrepancies (Art. 56 let. a LETO).

When must a bank report a discrepancy to the Transparency Register?

Where the discrepancy gives rise to doubts about the accuracy, completeness or currency of the information on the beneficial owner and persists despite a deadline set for the client (Art. 30 para. 1 LETA). The notification must be filed within 30 days (Art. 30 para. 2 LETA), and its content is governed by Art. 55 LETO.

What does beneficial ownership under the Transparency Act target?

Control over the company. A person is a beneficial owner if they control the legal entity with at least 25 percent of the capital or the votes, or control it in another manner (Art. 4 para. 1 LETA). Form A, by contrast, targets the beneficial owners of the assets held in the account in the case of a domiciliary company.

Does the Transparency Act recognise the concept of the domiciliary company?

No. The Transparency Act and its Ordinance do not adopt the anti-money-laundering category of the domiciliary company and determine the beneficial owner uniformly for every legal entity (Art. 4 LETA).

Are holding companies automatically domiciliary companies?

No. Holding companies that predominantly hold operating companies and whose purpose does not consist mainly in managing the assets of third parties do not qualify as domiciliary companies and are treated like operating companies (Art. 39 para. 4 let. b CDB 20).

Must the bank report every discrepancy to the Transparency Register?

No. Discrepancies arising from the special treatment of domiciliary companies under anti-money laundering legislation are expressly exempted from the notification obligation (Art. 56 let. a LETO).

Does the 25 percent threshold also apply to a domiciliary company?

Not under the CDB 20. The decisive factor is to whom the assets economically belong, irrespective of the size of the holding (Art. 27 para. 1 and 2 CDB 20). Under the Transparency Act, by contrast, the 25 percent threshold applies uniformly to all companies (Art. 4 LETA).

Which form does the bank require for a domiciliary company?

The bank requires a declaration by means of Form A as to who is the beneficial owner of the assets (Art. 39 para. 1 CDB 20). For operating companies, Form K applies instead (Art. 20 et seq. CDB 20).

What is a domiciliary company under the banks' code of conduct?

A domiciliary company is any Swiss or foreign legal entity, company, establishment, foundation, trust, fiduciary enterprise or similar association that is not operationally active (Art. 39 para. 2 CDB 20). Indications of this are the absence of business premises of its own or of staff of its own (Art. 39 para. 3 CDB 20).

Does a register extract replace the VSB 20 forms, in particular Form K?

No. An extract from the Transparency Register replaces neither Form A nor Form K under the CDB 20. The forms have different content from register extracts and bear the client’s signature. The register and the CDB forms have different legal bases and different functions; they complement each other.

Must discrepancies identified by banks, financial intermediaries and advisers relating to the chain of control always be notified under the Transparency Act (LETA)?

Not necessarily. Discrepancies in information relating to persons, legal entities or trusts that form part of the chain of control must only be notified if they give rise to concrete doubts as to the accuracy, completeness or currency of the information on the beneficial owners themselves (Art. 56 lit. c LETO).

Can the register-keeping authority suspend the access of banks, financial intermediaries and other advisers to information in the Transparency Register?

Yes. In the event of non-compliant use, the register-keeping authority may, after prior warning, suspend the access of the employee concerned (Art. 54 para. 5 LETO).

When does the obligation to notify discrepancies under the Transparency Act take effect?

The notification obligation under Art. 30 LETA does not take effect until six months after the Act enters into force (Art. 54 para. 1 of the LETA transitional provisions). Legal entities that are still within the two-year transitional registration period must confirm to financial intermediaries upon request that they are availing themselves of that period – otherwise the notification obligation applies.

What happens if a financial intermediary notifies a discrepancy under the Transparency Act (LETA) and it turns out to be unfounded?

A financial intermediary that files a notification in good faith is expressly exempt from liability for any breach of official, professional or business secrecy and for any contractual breach (Art. 30 para. 4 LETA). The notification must, however, be correctly reasoned and not submitted carelessly.

Are advisers under Art. 2 para. 3bis and 3ter AMLA required to notify discrepancies under the Transparency Act (LETA)?

No. The notification obligation under Art. 30 LETA applies only to financial intermediaries within the meaning of Art. 2 para. 2 and 3 AMLA. Advisers have the right to access the Transparency Register but are not subject to the discrepancy notification obligation.

Does the report to the transparency register replace banking forms such as Form K?

No. Extracts from the transparency register do not replace the forms provided for under the due diligence requirements of CDB 20. These have different content and must continue to be signed by the client.

What applies to the transparency register report if no one reaches the 25 per cent threshold?

If no natural person holds more than 25 per cent of the voting rights or capital, either directly or indirectly, and no control by other means is exercised, the most senior member of the governing body must be reported on a subsidiary basis (Art. 9 LETA).

Must fiduciary arrangements be disclosed in the report to the transparency register?

Yes. Anyone holding shares in a fiduciary capacity must disclose this — the legal classification is made under the criterion of “control by other means”.

When does the transitional period for initial reporting to the transparency register begin?

The period begins on the date the LETO enters into force, 1 October 2026, and runs for two years. Companies must therefore submit their initial report by the end of September 2028 at the latest (Art. 51 para. 2 LETA).

Where must companies keep the records relating to the beneficial owner available?

The documentation on the clarification of beneficial ownership must be accessible from Switzerland at all times, and for companies limited by shares and limited liability companies, the person authorised to represent the company and resident in Switzerland must have access to it (Art. 8 paras. 1 and 4 LETA).

Must unsuccessful clarification attempts also be documented under the LETA?

Yes. Where identification or verification proves impossible despite genuine efforts, this fact and the steps taken must be recorded in an appropriate manner (Art. 8 para. 2 LETA).

How long must records be retained under the LETA?

For ten years from the point in time at which the person concerned ceased to be a beneficial owner (Art. 8 para. 3 LETA). Records relating to former beneficial owners must therefore continue to be held.

Is it sufficient, for the purposes of documenting clarifications under the LETA, to maintain a list of beneficial owners?

No. In addition to identity data, the underlying clarifications and supporting documents must also be documented so that it is traceable how the company arrived at its determination (Art. 8 para. 1 LETA).

Can Konsento help prepare dividend confirmations and the bank payment file for a Swiss corporation?

Yes. After the dividend resolution has been passed in the general meeting, Konsento allows dividend confirmations to be generated for all dividend-entitled financial instruments in a few clicks, including the automatic deduction of the 35% withholding tax. The payment file for the bank (PAIN format) can also be prepared directly within the platform, based on the account details recorded for each shareholder and participant. This replaces a manually managed, error-prone process with a structured, fully documented workflow.

How does Konsento support the dividend process in Swiss corporations?

Konsento supports Swiss corporations throughout the entire dividend process. In the general meeting tool, shareholders can vote on dividend distributions using pre-built agenda item templates with calculation bases. After the resolution, Konsento enables the automated preparation of dividend confirmations for all dividend-entitled financial instruments — shares, participation certificates, and profit participation certificates — including the automatic calculation of withholding tax. Konsento also assists with generating the PAIN payment file for the bank and with recording the necessary account details for each shareholder and participant.

What is the difference between an advance dividend payment (Akontodividende) and an interim dividend in Swiss law?

The key difference lies in the legal basis. An interim dividend is a dividend properly resolved by the general meeting on the basis of interim financial statements. An advance dividend payment, by contrast, is not a validly resolved dividend, but an advance — or loan-like payment — made to shareholders in anticipation of a future dividend. If no dividend is subsequently resolved or the amount falls short of the advance, the shareholder is in principle required to repay the outstanding amount.

What are the requirements for an interim dividend in a Swiss corporation?

An interim dividend in a Swiss corporation requires interim financial statements as the basis for the general meeting's resolution (Art. 675a para. 1 CO). In principle, these statements must be reviewed by the statutory auditor before the resolution is passed (Art. 675a para. 2 CO). No review is required if the company is not subject to a limited statutory audit. A review may also be dispensed with if all shareholders consent and the claims of creditors are not jeopardised.

What legal requirements must be met before a dividend can be distributed in a Swiss corporation?

Under Swiss company law, dividends may only be paid out of net profit for the year and out of reserves created for this purpose (Art. 675 para. 2 CO). Before the board of directors submits a dividend proposal to the general meeting, it must verify that sufficient freely distributable funds are available, that the appropriate financial statements exist as a basis, and that any required review by the statutory auditor has been completed. The general meeting then formally resolves on the distribution.

Does the notification obligation also apply to beneficial owners who are not formal holders of equity interests?

Yes. Art. 14 LETA establishes independent notification and cooperation obligations for beneficial owners and third parties forming part of a chain of control. Anyone who controls a company through an intermediate structure without appearing directly as a holder of equity interests must, upon request by the company, supply the required information.

Que se passe-t-il si je viole intentionnellement mon obligation de communication ?

Les violations intentionnelles de l'obligation de communication peuvent être sanctionnées d'une amende de 500 000 francs au plus (art. 43 lit. a LTPM). L'autorité poursuivante est le Département fédéral des finances.

I have already notified under Art. 697j CO. Do I need to notify again?

Not necessarily. Anyone who has fully complied with the notification obligation under the existing law and where the person notified is also the beneficial owner under the new law is deemed to be exempt (Art. 49 para. 1 LETA). However, the company may request missing details — such as date of birth or nationality — which must be supplied within one month. If in doubt, a careful review of the existing notification is advisable.

How much time does a holder of equity interests have to notify the company of the beneficial owner?

The initial notification must be made within one month of the acquisition of control (Art. 13 para. 3 LETA). Changes must likewise be communicated within one month of the person subject to the notification obligation becoming aware of the change (Art. 13 para. 5 LETA).

To whom does a holder of equity interests address their notification?

The notification is made directly to the company — not to the transparency register. The company in turn is obliged to verify the information received and to notify the federal transparency register. The notification flow thus runs from the holder of equity interests through the company to the transparency register.

Does the notification obligation under the LETA apply to all shareholders?

No. The notification obligation applies only to persons who, alone or acting in concert with third parties, hold equity interests in an amount that enables ultimate control over the company. The relevant threshold is more than 25 percent of the capital or voting rights (Art. 13 para. 1 LETA).

How does Konsento help determine the correct beneficiaries of dividends?

Konsento uses the data maintained in the share register to determine the dividend-entitled holdings. The company can define a relevant record date and, on that basis, identify which shareholders and participants are to be considered and with which financial instruments.

How does Konsento support Swiss stock corporations with dividends?

Konsento supports Swiss stock corporations in structuring the preparation and operational execution of dividends. The company can determine the dividend-entitled holdings based on the share register, generate dividend statements, and calculate the relevant amounts in a transparent manner.

How are dividends distributed among shareholders?

Dividends are generally calculated in proportion to the amounts paid in on the share capital (Art. 661 CO). The articles of association may provide otherwise, for example through preferential rights. Therefore, it must be verified prior to distribution which participation rights are entitled to dividends and whether special provisions exist in the articles.

What is the role of the board of directors in a dividend distribution?

The board of directors prepares the proposal to the general meeting and must verify in advance whether the legal requirements for a dividend are met. This includes, in particular, verifying that sufficient freely distributable funds are available and that the proposal complies with the law and the articles of association.

Who decides on the distribution of a dividend?

The general meeting decides on the distribution of a dividend. This competence is inalienable and non-transferable (Art. 698 para. 2 no. 4 CO). The board of directors prepares the proposal but cannot validly resolve the dividend itself.

What happens in the event of incorrect filings?

Incorrect filings can lead to flags, in-depth preliminary reviews, formal control proceedings and ultimately to ordered measures (Art. 36 to 38 TJPG). They may also result in fines and reputational risks.

What is the role of the supervisory authority?

The supervisory authority reviews the accuracy, completeness and currency of the register entries on a risk-based or sampling basis and can order measures where necessary (Art. 35 and 38 TJPG).

What does a flag in the transparency register mean?

A flag indicates that there are doubts about the reported information or that a company has failed to comply with a request from the authority. It increases the risk profile of the company and may trigger further controls.

What is a difference report in the sense of the transparency act?

A difference report arises when authorities or financial intermediaries identify deviations between their own information and the data in the transparency register and notify the register-keeping authority (Art. 34 TJPG).

Is compliance with the reporting obligations to the transparency register actively monitored?

Yes. The Transparency Act provides for a multi-stage control system that reviews incoming filings, identifies deviations from other data sources and provides for risk-based controls by a specialised supervisory authority (Art. 33 et seq. TJPG).

How does Konsento support the review and revision of the articles of association?

Konsento accompanies the entire process, from analysing the existing articles through the revision itself to public notarisation at the general meeting. At its core lies a structured review of the key provisions on convocation, communications to shareholders, proxies, the virtual general meeting and the form of the shares.

Does a purely virtual general meeting need a basis in the articles of association?

Yes. Under Art. 701d CO, a general meeting held without a physical venue requires an express provision in the articles. Without such a basis, the board of directors may organise an in-person meeting with electronic participation (Art. 701c CO) but cannot dispense with a physical venue. Non-listed companies may, in addition, provide in their articles that no independent proxy needs to be appointed (Art. 704 para. 1 no. 15 CO), which considerably reduces the effort involved in running a lean virtual general meeting.

What does “in writing” mean in articles of association, and why can it become an obstacle to digitalisation?

Under Swiss law, “in writing” as a rule means paper bearing a handwritten signature or, where transmitted electronically, a qualified electronic signature (Art. 14 para. 2bis CO). If the articles require convocations of the general meeting, communications to shareholders or the granting of proxies to be made “in writing”, “by letter” or “by registered letter”, channels such as e-mail or platform-based solutions are effectively blocked. A formulation only becomes digitalisation-ready when the relevant form is supplemented by “or electronically”.

Is it enough to maintain the share register in digital form to dematerialise the shares?

No. Maintaining the share register digitally does not in itself eliminate a shareholder’s claim to receive a physical share certificate. In 2021, the Swiss Federal Supreme Court held that, without an express provision in the articles of association, a shareholder can successfully sue for the issuance of a share certificate. The articles must therefore clearly state that the shares exist exclusively as uncertificated securities or ledger-based securities (Art. 973c / 973d CO) and that the issuance of share certificates is excluded.

What if I cannot clearly verify the beneficial owner's identity?

In that case, this must be disclosed in the report and all available relevant information must be submitted, along with the most senior member of the governing body as the designated contact person (Art. 9 para. 3 LETA and Art. 12 LETO).

When does a control chain need to be reported?

The obligation is triggered in particular when a trust or at least two intermediate levels stand between the beneficial owner and the company, or when a fiduciary relationship forms part of the control chain (Art. 7 para. 1 LETO).

What is meant by control exercised in other ways?

This refers to situations in which control is not exercised through capital or voting right percentages, but for example through the right to appoint or remove the majority of board members, through veto rights, or through the right to determine profit distributions. The LETO requires a description of how that control is specifically exercised (Art. 3 and Art. 8 LETO).

Do I need to submit a change notification for every small share transfer?

Not necessarily. A change notification is triggered in particular when a transfer causes a reporting threshold to be crossed upward or downward (Art. 18 para. 3 LETO).

Do I need to report even if a single person holds 100 percent of the shares?

Yes. The reporting obligation applies even in the simplest of structures. What must be reported are identity data as well as information on the nature and extent of control (Art. 9 LETA in conjunction with Art. 6 LETO).

How does Konsento support the transfer of my company’s registered office in Switzerland?

Konsento supports you throughout the entire process of transferring your company’s registered office – from preparation to registration in the Commercial Register. The platform ensures that all legal steps are implemented correctly and efficiently. This includes preparing the shareholders’ meeting with a legally compliant agenda item for the transfer. The resolution can be adopted electronically via a written circulation process, enabling a lean and compliant execution. In addition, Konsento organises the notarisation through an online notary and prepares all required documents, including the amendment of the articles of association, the Commercial Register application and the certification of signatures of authorised representatives. Where required, a domicile declaration is also included. Finally, Konsento handles the submission and processing of the application with the Commercial Register, ensuring an efficient and legally secure process without media disruption.

What documents are required for a change of address?

A change of address requires: – A simple written application to the Commercial Register by the board of directors – If a c/o address is used: a declaration of domicile acceptance

What documents are required for a transfer of registered office?

The following documents must be submitted: – Public deed of the shareholders’ resolution – Updated certified articles of association – Commercial Register application signed by authorised signatories – Where applicable, a declaration of domicile acceptance

Does a change of address require notarisation?

No. A change of address within the same municipality only concerns the address and not the legal seat. It does not require an amendment of the articles of association and therefore no notarisation. A simple filing by the board of directors is sufficient.

Does a transfer of registered office require notarisation?

Yes. A transfer of registered office results in an amendment of the articles of association and must therefore be documented by a public deed, i.e. notarised (Art. 647 CO in conjunction with Art. 25 CommRegO).

Who decides on a transfer of registered office or a change of address in a Swiss company?

The shareholders’ meeting decides on a transfer of registered office to another municipality and this requires an amendment of the articles of association (Art. 698 para. 2 no. 1 CO). A change of address within the same municipality is decided by the board of directors (Art. 716a CO), as no amendment of the articles is required.

What is the difference between a transfer of registered office and a change of address in a Swiss company?

A transfer of registered office means moving the legal seat to another municipality. This requires an amendment of the articles of association and must be notarised. A change of address, by contrast, only affects the business address within the same municipality and does not require an amendment of the articles.

How does Konsento support the convening and execution of general meetings?

Konsento provides a digital platform for organizing, conducting, and automatically documenting general meetings. It helps ensure compliance with notice periods, enables legally compliant delivery of invitations, and automatically tracks receipt by shareholders. This reduces legal risks and allows you to run your general meeting efficiently, transparently, and with minimal effort.

What notice period applies to the general meeting of a Swiss corporation?

Swiss law requires a minimum notice period of 20 days for general meetings (Art. 700 CO). This period protects shareholder rights and ensures that shareholders have sufficient time to prepare. Failure to comply may result in the resolutions being challenged.

What is the principle of receipt for general meeting invitations?

The principle of receipt means that an invitation becomes legally effective only when it reaches the shareholder, i.e. enters their sphere of control and can be taken note of under normal circumstances. It is not necessary for the shareholder to actually read the invitation. The risk of delayed delivery lies with the company.

How do I correctly calculate the notice period for convening a general meeting?

The notice period is at least 20 days before the date of the general meeting (Art. 700 CO). Neither the day of the meeting nor the day of receipt of the invitation is counted. It is a full intermediate period. What matters is that the invitation reaches the shareholder no later than 20 days before the GM – not when it is sent.

Can subsequent contributions be carried out fully remotely with Konsento?

Yes, large parts of the process can be handled digitally and without unnecessary media discontinuities. This includes in particular the digital board resolution, online signatures, coordination of all parties and online notarisation.

What services does Konsento provide for subsequent contributions?

Konsento supports the entire process digitally: from the board resolution through templates, coordination with the bank and the notary, capital contribution account and reconciliation of payments through to commercial register filing and updating of the share register.

Is a notary required for subsequent contributions?

Yes, the completion of subsequent contributions generally includes a resolution subject to notarisation. Therefore, public notarisation by a notary is required before filing with the commercial register.

How are subsequent contributions carried out in practice?

As a rule, the obligated shareholders pay the outstanding amount into a capital contribution account. Subsequently, the payment is confirmed by the bank, the completion is determined by the board of directors, notarised and filed with the commercial register.

Who decides on subsequent contributions in a Swiss corporation?

Subsequent contributions are resolved by the board of directors. This is not a resolution of the general meeting, but a measure falling within the competence of the board of directors.

What added value does Konsento provide in relation to the exclusion of voting rights?

Konsento significantly reduces the risk of challengeable resolutions by implementing the exclusion of voting rights automatically at system level. Errors due to manual allocation or lack of awareness are avoided, and the general meeting can be conducted efficiently, transparently and in full legal compliance.

How does Konsento ensure that excluded shareholders cannot vote?

When setting up the general meeting in Konsento, shareholders who have participated in management can be technically excluded from voting on the discharge agenda item. These shareholders can still see the discharge item in the GM tool, but they are not given any voting options. This ensures that inadmissible votes cannot be cast.

Does the exclusion of voting rights also apply if a board member represents other shareholders?

Yes. The exclusion applies regardless of whether a board member votes in their own name or as a representative of other shareholders. What matters is who actually makes the voting decision. If a conflict of interest exists due to involvement in management, represented votes are also subject to the exclusion.

Who is excluded from voting on the discharge?

All persons who have participated in the management of the company in any way are excluded from voting (Art. 695 CO). This includes not only members of the board of directors, but also members of executive management, de facto governing bodies, and any other persons exercising significant influence over the company.

What are the legal limits of the discharge?

The effect of the discharge is clearly limited by law. It only covers disclosed facts (Art. 758 CO), does not bind creditors, and does not affect direct claims of individual shareholders (Art. 754 CO). In addition, shareholders who did not approve the discharge retain their right to bring claims for a transitional period of twelve months following the resolution (Art. 758 para. 2 CO).

What legal effect does the discharge have under Swiss law?

The discharge limits the enforcement of liability claims, but only with respect to disclosed facts and vis-à-vis a specific group of persons (Art. 758 CO). It is effective towards the company and shareholders who approved the discharge or who acquired their shares thereafter in knowledge of the resolution. It does not constitute a full waiver of liability.

What is the legal basis of the discharge of the board of directors?

The discharge is anchored in Swiss company law as a non-transferable power of the general meeting (Art. 698 CO). It is closely linked to the liability regime of the board of directors (Art. 754 CO) and the statutory provisions governing its effects (Art. 758 CO). Together, these rules define when and to what extent a discharge is legally relevant.

Can Konsento itself act as an independent proxy?

Yes. Upon request, Konsento can assume the role of independent proxy in general meetings conducted on the platform. This naturally only occurs where the legal requirements for independence are fulfilled.

Can a representative be explicitly designated as an independent proxy in Konsento?

Yes. In Konsento, representatives can be explicitly marked as independent proxies. This information is visible to shareholders in the general meeting interface and helps them choose an appropriate representative. The designation is also reflected in the voting results and in the automatically generated minutes.

Why is it useful for the board of directors of a non-listed corporation to proactively appoint an independent proxy if the articles of association provide that shareholders may only be represented by other shareholders at the general meeting?

Especially in companies with many shareholders, shareholders often do not know each other and generally have no easy way of contacting other shareholders to ask them to represent them at the general meeting. Even if some contact exists, it would hardly be reasonable to expect shareholders to make significant efforts to organise representation. From the shareholders’ perspective, it is therefore much more practical if the board of directors provides an independent proxy from the outset.

What is the benefit for shareholders if the board of directors appoints an independent proxy?

Such a voluntary solution can be particularly useful if several shareholders are unable to attend the general meeting in person or if the board of directors wishes to ensure neutral and transparent voting representation.

Can the board of directors of a non-listed company always nominate an independent proxy?

Yes. The board of directors of a non-listed corporation may also appoint an independent proxy voluntarily, even if there is no legal obligation to do so. If an independent proxy is appointed voluntarily, care should be taken to ensure that the person is genuinely independent and that no conflicts of interest exist. This corresponds to the purpose of the legal rules governing the independent proxy (Art. 689c–689d CO).

How does Konsento support proxy voting at the general meeting?

In the general meeting tool of Konsento, proxies can easily be recorded and managed. Proxies can also be explicitly designated as independent proxies. This information is visible to shareholders in the meeting tool and enables a transparent selection of the desired proxy. During the general meeting, the proxy’s status is clearly indicated: in the overview of represented votes, in the voting results, and in the automatically generated minutes. Upon request, Konsento may also act as the independent proxy at general meetings, naturally only where the statutory independence requirements are fulfilled.

May an independent proxy be economically dependent on the company?

Economic dependence may impair independence (Art. 728 para. 2 no. 5 CO). This may be the case, for example, if an adviser or trustee derives a substantial portion of their income from mandates with the company. According to the ExpertSuisse independence guidelines, economic dependence is often assumed where a single client accounts for around 30% or more of annual revenues over several years. Although this threshold does not directly apply to independent proxies, it illustrates the underlying principle: a person who is economically dependent on the goodwill of the company is unlikely to be perceived as fully independent.

When can a financial interest compromise independence?

Independence may be impaired if the proxy holds a direct or significant indirect shareholding in the company (Art. 728 para. 2 no. 2 CO). An indirect participation may arise, for example, through a holding company, an investment fund or a related entity. The law does not define specific thresholds. In practice, however, reference is often made to the independence guidelines issued by ExpertSuisse. These guidelines generally consider an indirect financial interest to be significant if it exceeds approximately 10% of the person’s equity or net assets. While this threshold does not directly apply to independent proxies, it provides a useful indication.

What does “independence” mean for an independent proxy?

The independence of the independent proxy must not be impaired either in fact or in appearance (Art. 689b para. 4 CO). To clarify this requirement, the law refers to the independence rules applicable to statutory auditors (Art. 728 paras. 2–6 CO). These rules are intended to ensure that the proxy exercises the shareholders’ voting rights in a neutral manner and without conflicts of interest. Particularly problematic are close organisational, economic or personal relationships with the company or with its decision-makers.

When must a non-listed Swiss company appoint an independent proxy?

A non-listed Swiss corporation must appoint an independent proxy if its articles of association provide that shareholders may be represented at the general meeting only by other shareholders (Art. 689d para. 1 Swiss Code of Obligations). In such a case, a shareholder may request that the board of directors designate an additional representative to whom shareholders may delegate their voting rights. This may be either an independent proxy or a corporate proxy (Art. 689d para. 2 CO). However, corporations may also appoint an independent proxy voluntarily at any time. The board of directors must inform shareholders no later than ten days before the general meeting whom they may appoint as their proxy (Art. 689d para. 3 CO).

Can AGM minutes be digitally signed and archived in Konsento?

Yes. AGM minutes can be signed directly in Konsento using a qualified electronic signature. Alternatively, they can be exported as a PDF, signed by hand, and then uploaded back into Konsento. In both cases, the documents can be securely archived and shared with the shareholders.

Wie hilft Konsento kleinen Aktiengesellschaften bei der Erstellung eines GV-Protokolls?

Konsento erstellt für kleine Aktiengesellschaften mit bis zu drei Aktionären automatisch eine sogenannte GV-Schnellversion. Daraus kann mit wenigen Klicks ein vollständiges, rechtskonformes Protokoll der Generalversammlung erstellt werden, ohne dass Traktanden manuell vorbereitet oder Abstimmungen organisiert werden müssen

What information must be included in the minutes of the General Meeting?

Swiss company law defines a minimum content for the minutes of the General Meeting. This includes, in particular, the resolutions adopted by the General Meeting as well as the results of votes and elections. In practice, AGM minutes also contain information about the number of shares and voting rights represented at the meeting, as well as the agenda items that were discussed.

Who must sign the minutes of the General Meeting?

The minutes of the General Meeting must be signed by the chair of the General Meeting and the minute-taker (Art. 702 para. 3 CO). These roles may also be performed by the same person. The minutes can be signed either by handwritten signature or by means of a qualified electronic signature.

Must every Swiss corporation prepare minutes of the General Meeting?

Yes. Swiss company law requires every corporation, regardless of its size or the number of shareholders, to hold an ordinary General Meeting once a year and to record minutes of every General Meeting (Art. 702 CO). The minutes serve as the official record of the resolutions adopted and are an important document for the company’s corporate governance.

How does the concept of control under the Transparency Act (for reporting to the Transparency Register) differ from the concept of control under the Investment Screening Act (IPG)?

The two concepts of control serve different purposes and differ both in their structure and in their practical application. Under the Transparency Act, the aim is to identify natural persons who actually control a company — that is, those who exercise direct or indirect decisive influence and therefore must be reported in the Transparency Register (Transparency Act Art. 2–3 TJPV). Control by shareholding: A natural person controls a company if they directly or indirectly hold at least 25 % of the capital or voting rights (Art. 2 para. 1 TJPV). Control in other ways: A natural person also controls a company if, for example, they can appoint more than half of the board members, have a veto over decisions, or otherwise exert decisive influence (Art. 3 para. 1–2 TJPV). The Transparency Act therefore adopts a relatively broad concept of control that considers both shareholding thresholds and other avenues of influence to determine who actually governs the company. By contrast, the Investment Screening Act (IPG) defines control not with a view to natural persons, but in connection with takeovers by investors. Control in the IPG context means that an investor directly or indirectly acquires control over a company, typically through a merger, the acquisition of a stake, or the conclusion of a contract (Art. 2 lit. a IPG). The decisive point here is that a previously independent company can be economically and legally dominated by an investor. The focus is on the entry of the investor into a dominant position, not on identifying individual controlling persons.

How can companies already prepare today for the reporting obligations under the Transparency Act?

Companies can prepare effectively by clarifying and documenting their ownership structure at an early stage. This includes identifying the beneficial owners and systematically recording the relevant information. Early preparation reduces time pressure, minimises errors and significantly facilitates later reporting to the transparency register.

Can a change in the commercial register trigger the reporting deadline earlier?

Yes. A first change entered in the commercial register after the entry into force of the Transparency Act may trigger the reporting deadline independently of the general transitional period. In such cases, the reporting period begins with that change, even if the ordinary transitional period has not yet expired. Companies should therefore carefully plan any commercial register changes after the Act enters into force.

Which transitional periods apply to the reporting of beneficial owners to the transparency register?

The Transparency Act does not provide for a single uniform transitional period. The applicable deadlines depend on the legal form, audit status and complexity of the ownership structure. In simple cases where all beneficial owners are already identifiable from the commercial register, a transitional period of up to two years applies. In all other cases, significantly shorter deadlines of three to six months apply.

From when does the reporting obligation to the transparency register apply under the Transparency Act (TJPG)?

The reporting obligation to the transparency register generally arises upon the entry into force of the Transparency Act (TJPG). From that date, obliged legal entities must identify, document and report their beneficial owners to the transparency register within the statutory deadlines. The obligation arises automatically by operation of law and does not depend on a prior request by the authorities.

What needs to be done with the existing register of beneficial owners?

The existing register of beneficial owners remains relevant under the Transparency Act. Information already collected and documented under current law can generally continue to be used, provided that it complies with the new legal requirements and is up to date. In addition, such records must be retained for ten years. Companies should therefore review, update and archive their existing register in an audit-proof manner.

Why does the board of directors need specific regulations for holding general meetings using electronic means?

The board of directors’ regulations specify the statutory requirements for virtual or hybrid general meetings and ensure that such meetings are conducted in compliance with the law. They set out in a binding manner how electronic means are to be used, which organisational and technical requirements apply and how shareholders’ rights are safeguarded. The regulations therefore provide legal certainty for the board of directors and transparency for the shareholders.

Which matters must the board of directors’ regulations on the use of electronic means at the general meeting specifically address?

The regulations must define how the identity of shareholders participating electronically is clearly established. They must also ensure that statements can be made immediately and without filtering during the discussion of the relevant agenda items. In addition, the regulations must govern the right of all participants to submit motions and take part in discussions, as well as the correct and unaltered determination of voting results, in particular to prevent multiple or contradictory exercises of voting rights in the case of electronic participation.

Our latest posts

Dividends in Swiss Corporations: Types of Distribution and Legal Requirements

A dividend is the distribution of profit or freely distributable reserves to shareholders. This article explains the most important types of dividend in Swiss corporations and shows how cash dividends, non-cash dividends, ordinary, extraordinary, interim, and advance dividends differ from one another. It sets out the applicable legal framework under Swiss company law and explains the practical implications for boards of directors and Swiss SMEs.

Dividend Distribution in a Swiss Corporation: How Dividend Payments Are Carried Out

Dividend distribution begins with the annual financial statements and the board of directors’ proposal to the general meeting. This article explains the role of freely distributable funds, the statutory auditor and the general meeting resolution. It then shows how dividends are calculated and how withholding tax is handled. Finally, it outlines how Konsento supports the creation of dividend confirmations.

Digitalisation-Ready Articles of Association: Which Provisions Slow Down Digital Corporate Governance

Many stock corporations hold their general meetings virtually and dematerialise their shares without their articles of association reflecting this approach. This article shows which formulations on convocation, communications, proxies, the virtual general meeting and the form of shares typically stand in the way of digitalisation. It draws on the relevant provisions of the revised Swiss company law (Art. 626, 689, 700, 701a et seq., 973c, 973d CO) and on the case law of the Swiss Federal Supreme Court regarding the right to physical share certificates. It closes with a practical overview of what distinguishes digitalisation-ready articles of association today.

Which formats of general meetings are recognised under Swiss law?

Swiss corporate law offers a wide range of formats for general meetings – from traditional in-person meetings to fully digital and written resolutions. But which format is legally permissible? What role do the articles of association play? And what requirements must be met in practice? This article provides a structured overview and practical guidance for companies.

Interview with the CANTREAT Founders: Focus on Cancer Research Instead of Administration – How CANTREAT Keeps Its Back Free

In this interview, the CANTREAT founding team shares insights into their vision, the challenges of a rapidly growing shareholder structure and how they handle increasing corporate governance complexity. They explain why administrative processes can quickly become a bottleneck—and how Konsento helps create clarity, save time and elevate governance standards.

CANTREAT AG – Fighting Cancer with Precision: How a MedTech Startup is Rethinking Tumor Treatment

How do you combine high-precision MedTech innovation with a complex shareholder structure? CANTREAT AG shows how it’s done. While the startup is rethinking cancer treatment with magnetically controlled nanoparticles, Konsento ensures clear, efficient and legally compliant processes in the background—from digital share register to general meetings and capital measures. This allows CANTREAT to fully focus on research, development and growth.